There are two significant metrics in the world of corporate finance and investment valuation, which are FCFF (Free Cash Flow to the Firm) and FCFE (Free Cash Flow to Equity). These are some of the most effective tools that analysts employ to establish the real value of a company and its capacity to earn money to the investors.

Whether you’re a finance student, an investor, or a business owner, understanding FCFF and FCFE helps you see beyond accounting profits to the company’s real financial health.

Let’s break everything down in simple terms.

What Is Free Cash Flow?

Free Cash Flow (FCF) is the amount of cash that a company can generate after it has paid all the operating expenses and capital investments.

In simple words, it’s the money left over to:

- Pay back lenders, and

- Distribute dividends to shareholders.

Depending on who the cash belongs to, we can divide it into:

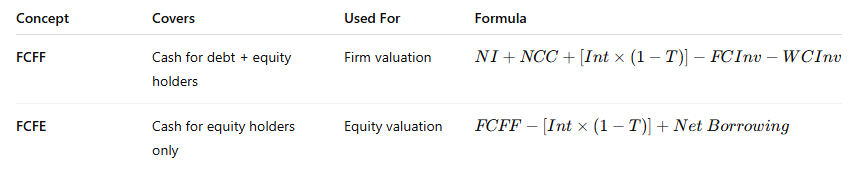

- FCFF (Free Cash Flow to the Firm) — for both debt and equity holders.

- FCFE (Free Cash Flow to Equity) — only for shareholders.

What Is FCFF (Free Cash Flow to the Firm)?

FCFF measures the cash flow available to all investors (both debt and equity holders) after all operating expenses, taxes, and investments in working capital and fixed assets are accounted for.

It shows how much cash the company generates before making interest payments.

FCFF Formula (from Net Income)

Where:

- NI = Net Income

- NCC = Non-cash charges (Depreciation, Amortization, etc.)

- Int = Interest Expense

- FCInv = Fixed Capital Investment (Capital Expenditure)

- WCInv = Working Capital Investment

Alternative FCFF Formulas

From EBIT (Earnings Before Interest and Taxes)

From EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization)

Each version leads to the same result — the difference lies in where you start the calculation.

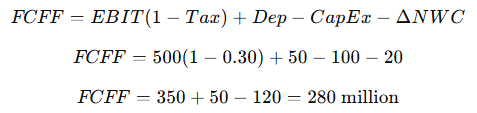

Example: Calculating FCFF

Let’s take an example to make things crystal clear.

| Item | Value |

|---|---|

| EBIT | $500 million |

| Tax Rate | 30% |

| Depreciation | $50 million |

| CapEx | $100 million |

| Change in Working Capital | $20 million |

Now, apply the EBIT-based formula:

FCFF = $280 million

This means the company generated $280 million in free cash available to both its debt and equity investors.

What Is FCFE (Free Cash Flow to Equity)?

FCFE measures the amount of cash available only to the company’s shareholders after accounting for debt payments and new borrowings.

It’s the money that could be potentially paid out as dividends or used to repurchase shares.

FCFE Formula

Where:

- Net Borrowing = New Debt Issued – Debt Repaid

This formula removes the interest portion (since it belongs to lenders) and adds new borrowings (which increase the equity holder’s share of cash).

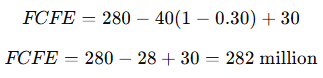

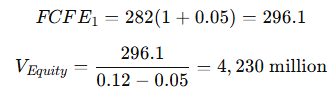

Example: Calculating FCFE

Using the FCFF we calculated earlier ($280 million):

| Item | Value |

|---|---|

| FCFF | $280 million |

| Interest Expense | $40 million |

| Tax Rate | 30% |

| Net Borrowing | $30 million |

Now plug in the values:

FCFE = $282 million

This is the cash available for shareholders after meeting all obligations.

Valuation Connection

Now that we’ve calculated FCFF and FCFE, we can use them to estimate the value of the firm and the value of equity.

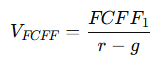

Value of the Firm (Using FCFF)

Where:

- FCFF1 = next year’s expected FCFF

- r = required return or WACC (Weighted Average Cost of Capital)

- g = long-term growth rate of FCF

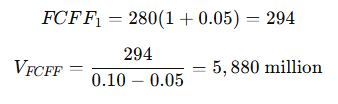

Example:

If current FCFF = $280 million,

growth rate, g = 5%,

and WACC, r = 10%

Firm Value = $5.88 billion

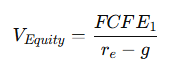

Value of Equity (Using FCFE)

Where:

- re = cost of equity

Example:

If current FCFE = $282 million,

growth rate, g = 5%

and cost of equity, re = 12%

Relationship Between FCFF and FCFE

In short:

→ FCFF values the entire business,

→ FCFE values shareholders’ ownership.

Key Takeaways

- FCFF tells you how much cash the company generates for both debt and equity holders.

- FCFE focuses only on what’s left for shareholders.

- Both can be used in valuation models to estimate firm or equity value.

- The formulas connect through interest and net borrowing adjustments.

- FCFF uses WACC for discounting; FCFE uses cost of equity.

Final Thoughts

Understanding FCFF and FCFE bridges the gap between accounting earnings and actual cash performance.

For investors, these cash flows reveal how much value a company truly creates — not just on paper, but in reality.

When applied correctly, FCFF and FCFE form the foundation of Discounted Cash Flow (DCF) valuation, one of the most respected methods in modern finance.